Grid+Storage regional workshop: Baltics

|

Research & Innovation activities 12-13 January 2016

|

|

|

|

|

|

Research & Innovation activities 12-13 January 2016

|

|

|

|

|

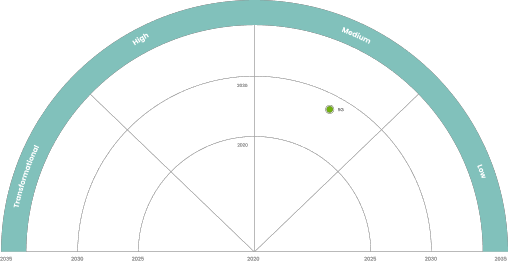

5G is the next generation wireless network technology. This will be faster and able to handle more connected devices than the existing 4G LTE network. Key benefits of 5G are Ultra low latency (~1ms vs. 100ms for 4G), Speed (Higher than 1Gbps vs. 100Mbps for 4G) and Connectivity (~1’000’000 devices / km2 vs. 100’000 for 4G). These developments are accompanied by disruptive technological choices opening up new possibilities:

Since 2022, all European countries have a commercial 5G service available at least in a part of the country. Close to 256’074 5G base stations are now active in the EU and approximately 72% of the EU’s population is covered by at least one 5G network

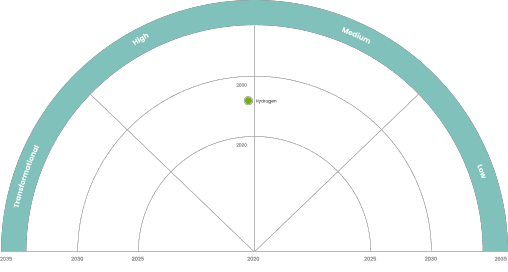

Today, hydrogen (H2) is almost exclusively used in industry, especially the chemical industry, metallurgy and refining. Currently, it is 96% produced from fossil fuels. Recent technological advances have improved the yields and reliability of water electrolysis processes. Hydrogen can thus be produced from decarbonized or renewable electricity. As a consequence, the significant role of the hydrogen sector in the decarbonization of the economy through its chaining with the electricity sector leads DSOs to study the impact of the development and integration of H2 technologies and systems (electrolysers, storage, fuel cells in particular) in the electricity system.

To meet the full projected hydrogen demand in Europe by 2050 (2150 - 2750 TWh), it would take about 2900 - 3800 TWh of electricity. Despite announcements of gigawatts of electrolysers being installed over the next decade, operational electrolyser capacity is yet to reach 100 MW across Europe. While 48% of European electrolyser capacity is in Germany, no other country has more than 10 MW installed as of today. Around one third of the installed capacity is providing some form of ancillary service to the electricity system.

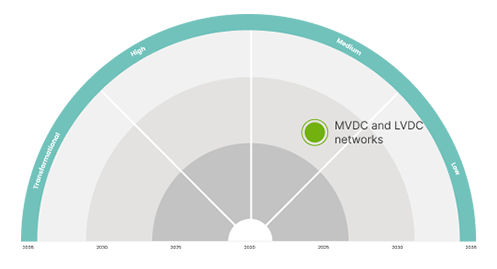

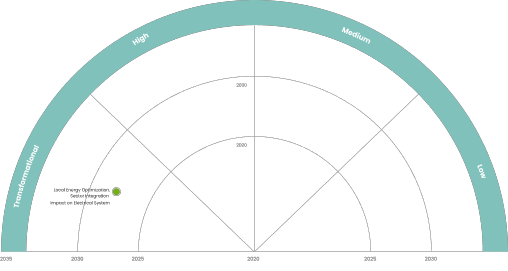

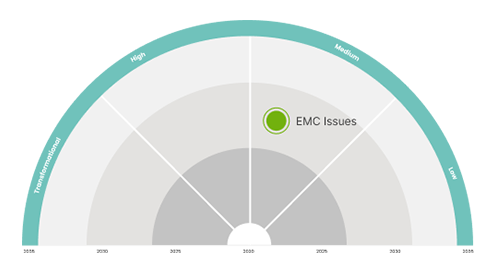

Although the transmission and distribution of electricity is almost exclusively carried out in alternating current (AC), certain trends call for a reconsideration of the interest of direct current (DC): (1) renewable energies (PV and wind) and batteries (in particular EV) operate natively in DC, and the acceleration of renewable energies reinforces this interest, (2) the proportion of energy consumed in DC in the home is high (50% in 2018) and growing sharply ( 80% by 2030) and (3) innovation and falling costs in power electronics are making the use of DC increasingly economical. The use of direct current could make it possible to limit conversions on the distribution network, be a source of simplification and improve the energy efficiency of the electrical system.

DC solutions, in particular for the distribution network, are arising great interest, with numerous demonstrators around the world and, it seems, a proactive industrial policy in China.

Standardization of DC networks is of critical importance (even more for LVDC to enable development of appliances). The International Electrotechnical Commission (IEC), and Institute of Electrical and Electronics Engineers (IEEE) have all started standardization work on MV and LV DC networks.

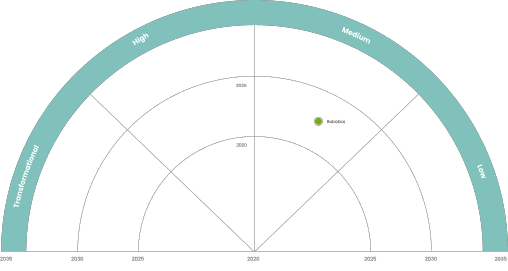

Robotics is used in multiple fields (industrial, agricultural, domestic, scientific, educational, medical, military, leisure, service, transport robotics, etc.). It is a science of technological integration at the crossroads of mechanics, electronics, computer science and networks, in particular communication. The desire to relocate production to Western countries and the ageing of the population are drivers of the revival of robotics, especially since the key technologies of robotics are experiencing spectacular advances: the rise of artificial intelligence, the sophistication of sensors, improved battery efficiency, IoT, 5G, etc.

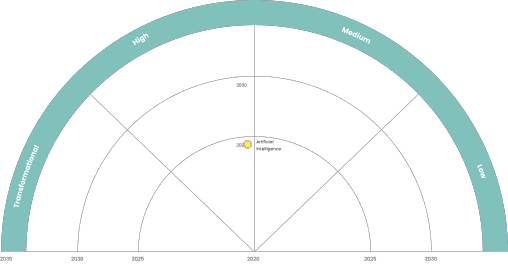

Artificial Intelligence (AI) is an interdisciplinary field that combines theory and practice. It is about assisting human activities, mainly via software and, in some cases, even replacing them. AI involves the use of information systems, data within management systems and dedicated algorithms. AI performance is based on the combination of the availability of a large amount of data, large computing capacity, and machine learning algorithms. As distribution networks are generating a growing amount of data, due to the deployment of smart meters and increased measurement and communication capabilities, DSOs have early on considered AI solutions.

For the European Parliament, artificial intelligence represents any tool used by a machine to "reproduce human-related behaviours, such as reasoning, planning and creativity". The AI Act is a proposed European law on artificial intelligence – the first law on AI by a major regulator anywhere. The law assigns applications of AI to three risk categories. First, applications and systems that create an unacceptable risk are banned. Second, high-risk applications are subject to specific legal requirements. Lastly, applications not explicitly banned or listed as high-risk are largely left unregulated.

The kinetic energy of synchronous rotating machines is crucial for the stability of the power system. Current grid control and backup methods are based on this physical characteristic. In the case of solar and wind power plants, the production is injected into the grid through electronic circuits that have no inertia and therefore do not contribute to grid stability. As a consequence, the massive development of renewable energy solutions and other resources connected by power electronics leads to a decrease in the share of synchronous rotating machines in the electrical system that will cause a change in grid control and backup methods.

Today, the inverters of renewable energies behave in a grid-following way. They synchronize themselves with the grid to produce the desired active and reactive power (depending on the primary resource). Depending on the connection level and requirements, they can “support" the grid by providing certain system services (voltage). European grid codes require some new groups to know how to provide system service frequency which requires grid-forming inverters (and other smart functions: reactive power at night, etc.).

Challenges and opportunities for DSOs

EDSO Considerations

More information will be available soon...

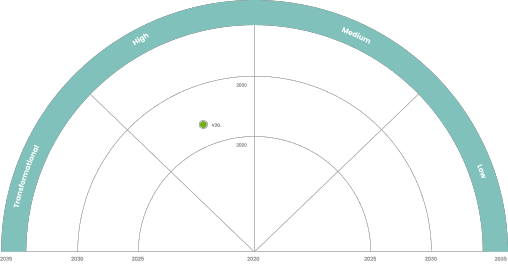

The concept of Vehicle-to-Grid (V2G) is very similar to the one of smart charging. Smart charging, also known as V1G, allows deciding how much capacity/energy to allocate to Electric Vehicle (EV) charging in real-time. V2G solutions go further and add the ability to redirect energy from a battery to the power grid to balance the network, especially when demand suddenly increases. Vehicle-to-Everything (V2X) is not very different from V2G and includes V2H (Vehicle-to-Home), V2B (Vehicle-to-Building), and V2G.

The transportation sector is undergoing a revolution that can be seen in the growing number of electric vehicles on our roads. In addition to having a much smaller ecological footprint than combustion vehicles, electric car batteries represent an energy storage option. Globally, 140 to 240 million electric vehicles are expected to be on the road by 2030. That means there will be at least 140 million energy sources on wheels, totalling about 7 TWh of storage capacity. Today, only a few models are compatible with V2G technology. New (distributed) energy sources like V2G are challenged to compete in traditional energy markets that are not fully aligned with their capabilities. Energy regulation is complex and provides an obstacle for emerging technologies like smart car charging and V2G to make an immediate impact.

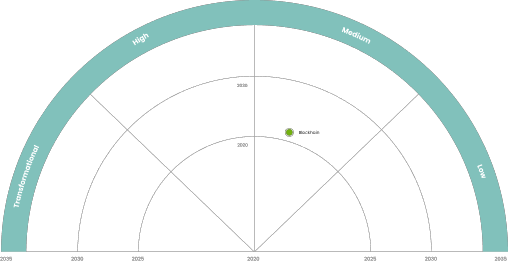

Blockchain is a transparent, secure information storage and transmission technology. It is a secure, distributed database containing the history of all exchanges made between its users since its creation: it is shared by its various users, without intermediaries, enabling everyone to check the validity of the chain. There are public blockchains, open to all, and private blockchains, whose access and use are limited to a certain number of players. In addition to cryptocurrencies, blockchain has numerous applications in the supply chain, healthcare, digital identity, asset transfer (real estate titles, shares, bonds, etc.), the Internet of Things, etc. Democratisation and decentralisation of the utility marketplace could be a key driver for the adoption of blockchain.

In 2021, the total spending on various blockchain solutions worldwide reached $6.6 billion. According to Statista, the global spending will reach nearly $19 billion by 2024. However, the commercial added value of the technology could be much higher, reaching $176 billion by 2025 and exceeding $3.1 trillion by 2030, according to Gartner estimates. In 2017, a McKinsey study determined that blockchain could increase industry productivity by up to 9% and boost cost savings by 7%, all by simply improving progress tracking and the accuracy of cost and schedule estimates.

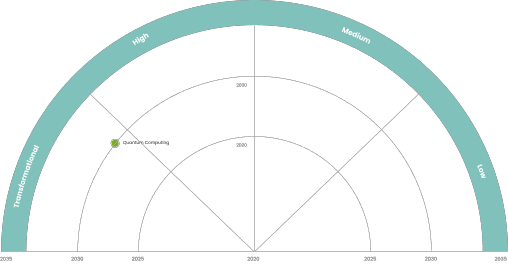

Quantum computing uses the quantum properties of matter (superposition states, interference and entanglement) to perform calculations with qubits. To this end, four technologies are competing: superconduction qubits, silicon qubits, trapped ion qubits and photonic qubits. As a universal quantum computer is not yet available, industry is working with researchers to create quantum computers adapted to useful problems, and thus benefit from a real quantum advantage. Within the next 10 years, quantum computing will revolutionize a number of fields: simulation, optimization, machine learning and cryptography.

As of 2023, GAFAM and numerous start-ups are offering Quantum Computing-as-a-Service to demystify quantum computing. The quantum advantage should be indisputable within 5 years and this explains the interest shown by governments and the funds raised in start-ups. By way of example, start-ups Pasqal (France) and IQM (Finland) raised respectively €100 million and €128 million in 2022. The risks posed by the development of quantum in the cybersecurity policy of DSOs require them to take an interest in these technologies.

More information will be available soon...

More information will be available soon...

More information will be available soon...

More information will be available soon...

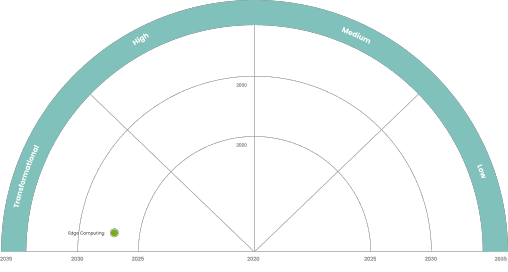

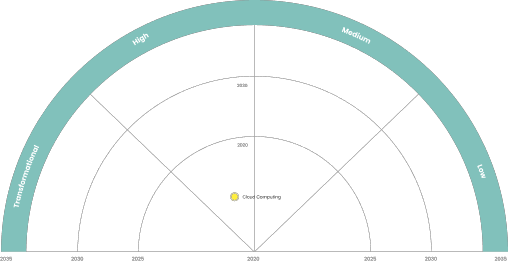

Edge computing refers to a distributed computing architecture that is characterized by decentralized processing power. In concrete terms, edge computing allows data to be processed directly by the device that produces it or by a local computer. In this case, it is no longer necessary to transmit the data to a remote data centre to analyze it. Edge computing enables data to be processed in real-time and in large quantities as close as possible to its source, with reduced bandwidth usage, lower latency and the necessary security layer for sensitive data. This technology is mainly found in the field of IoT, where it competes with cloud computing.

Edge computing is evolving as new technologies such as artificial intelligence and machine learning bring new data analysis capabilities to the table, and emerging business models such as IoT as a service enable solution providers to deliver innovative offerings in new ways. With an average increase of 16% per year, spending on Edge Computing totalled $40 billion in 2022 in Europe and should reach $64 billion in 2025. Service providers, editors and manufacturers are sharpening their offers to meet the growing demand from companies.

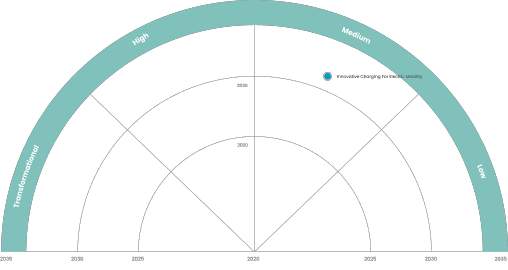

To get around the constraints of wired charging, innovative charging solutions for electric mobility are being researched and experimented. Static and dynamic wireless charging solutions at urban and high-speed operation are being tested in Europe, Asia and the USA:

Dynamic charging solutions involve significant investment costs for road infrastructure which is a significant drawback for massive road projects.

Dynamic charging will be distributed over long distances and effectively be connected to several points in the grid. Considering inductive charging, the efficiency of the energy flow is comparable to the typical efficiency of fast charging. To limit power losses and facilitate integration with renewable energy sources, inductive solutions are generally DC-based.

If DC solutions are adopted:

Some metals cooled to very low temperatures (typically between -272 and -240°C) acquire the superconducting state, i.e. the ability to conduct electric current without resistance and, thus, without energy loss. Superconductivity has reached the industrial stage in some sectors for the production of intense magnetic fields such as medical imaging, particle accelerators and tokamaks. The applications of superconductivity to grid cables and current limiters have been the subject of experiments after the discovery in the mid-1980s of "high temperature" superconductivity (-196°C) which allows the use of liquid nitrogen for cryogenic purposes. Superconducting cables carry up to 5 times more energy than standard cables.

Tests have been conducted over the past fifteen years (Long Island 2008: 600 m, 138 kV, 574 MW; Essen 2014: 1000 m, 10 kV, 40 MW). Links have recently been put into service or are planned: Shingal/Korea 2019: 1000 m, 23 k, 50 MW; Shanghai 2021: 1200 m, 35 kV, 80 MW; Chicago 2021: ~ 100 m, 12 kV, 62 MW; Paris/Gare Montparnasse link project, 2 links of 80m, 1500V DC, 5MW). Experiments with current limiters (10 kV to 138 kV, from a few MVA to a few tens of MVA) have taken place in the USA, Asia (Korea, Japan, China), Germany and the United Kingdom since the 2010s, without leading to the deployment of these solutions.

A microgrid is a group of interconnected loads and distributed energy resources with defined electrical boundaries forming a local electric power system at distribution voltage levels, that acts as a single controllable entity and is capable of operating in island mode, no matter if it is standalone or grid-connected (IEC 62898). When operating in islanded mode, microgrids can manage and optimise supply and demand (energy management system) and regulate demand locally. When operating in connected mode they may also aim to offer new services (provision of flexibilities, congestion management, reactive power management, etc.). The main objectives of microgrids are to improve resilience and decarbonize production.

During periods when they are disconnected from the grid, microgrids operate in the same way as islands and isolated sites, which always had to produce their own electricity. Today, the strong development of renewable energy represents an opportunity to make these installations less costly and more respectful of the environment. The global microgrid market is expected to grow at a high annual rate (estimated at 10% in Europe over the period 2022-2030). Market growth is driven by the need to incorporate renewable energy and the rapid adoption of electric vehicles as well as high energy prices. Furthermore, the threat of cyber-attacks, climate hazards and geopolitical developments are stimulating the desire for energy independence.

More information will be available soon...

More information will be available soon...

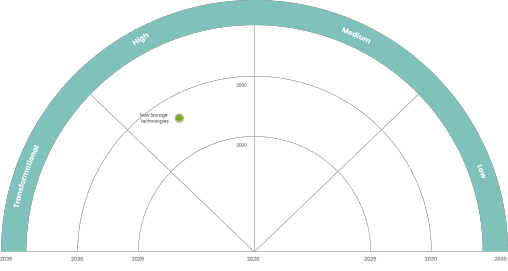

Efficient energy storage technology is needed to overcome fluctuations in renewable energy supply and decrease our reliance on fossil fuels. Storage could provide important system services that range from short-term balancing and operating reserves, ancillary services for grid stability to long-term energy storage and restoring grid operations following a blackout. Storage can help manage congestion and voltage at different timescales in the distribution network. In some cases, it could defer or even reduce the need to reinforce the network.

Pumped-storage hydropower is the most widely used storage technology. Batteries are the most scalable type of grid-scale storage and the market has seen their strong growth in recent years. Other storage technologies include compressed air, gravity storage, superconducting magnetic energy storage, flywheels and hydrogen but these play a comparatively small role in current power systems. Up to date, apart from pumped-storage hydropower, technologies that allow for inter-seasonal or even inter-annual storage are not yet mature. The scarcity and environmental concerns related to raw materials needed to manufacture storage solutions need to be taken into account, particularly for batteries. Article 36 of the Electricity Directive restricts DSOs from owning, developing, managing or operating storage facilities, although some exceptions are possible due to efficient, reliable, safe operations etc.

More information will be available soon...

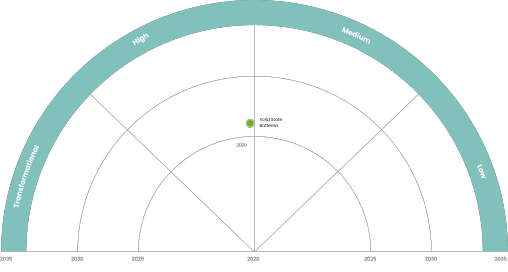

A solid-state battery uses solid electrodes and electrolytes, rather than the liquid electrolytes or polymer gels found in lithium-ion or lithium-polymer batteries. Solid-state batteries promise higher energy density than Li-ion batteries, which use a liquid electrolyte solution, as well as increased fast charging capabilities. They also entail no risk of explosion or fire, so there is no need for safety components, saving space. Worldwide efforts to make solid-state batteries a potentially safe and stable high-energy, high-throughput electrochemical storage technology are still hampered by problems of long-term performance, specific power and economic viability.

More information will be available soon...

More information will be available soon...

More information will be available soon...

3D printing enables the production of complex designs and shapes. Initial limits of 3D printings have been pushed back, both in the size of the objects to be produced and in the materials used (stainless steel, plastic, glass, metal, concrete, eco-materials, etc.). However, despite these advancements, the technology still faces significant challenges, including high costs, low printing speed, limited part sizes, and strength.

The European 3D Printing Market was valued at USD 4.61 billion in 2020 and is expected to reach USD 10.12 billion by 2026. The highest demand in Europe comes from small and medium-sized businesses that are in need of high-speed, reliable and low-cost prototypes. This concerns numerous sectors, particularly automotive, healthcare, aerospace along with defence.

More information will be available soon...

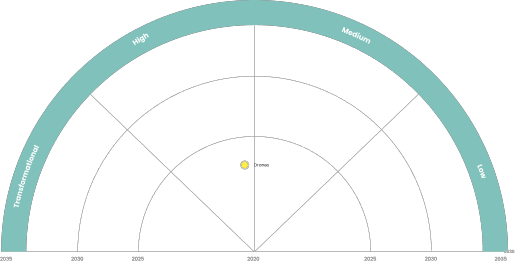

Originally developed for military applications, drones have found their way into many fields due to the improved levels of safety and efficiency they bring. These robotic Unmanned Aerial Vehicles (UAVs) operate without a pilot on board and with different levels of autonomy. Initially focused on image capture, their uses are set to expand thanks to the expected progress in drone systems (ability to fly longer distances), AI (image processing, guidance, etc.), sensors (miniaturisation of lidar, etc.), telecommunication (5G, etc.), technical action capabilities (manipulator arms, etc.). The development of the use of drones is highly dependent on regulation, which lays down strict rules that vary considerably depending on whether or not the operator is flying within sight of the UAV.

The European Drone Strategy 2.0 sets out a vision for the further development of the European drone market. It builds on the European safety framework for operating and setting the technical requirements of drones. The new Strategy lays out how Europe can pursue large-scale commercial drone operations while offering new opportunities in the sector. The Strategy envisions the following drone services becoming part of European life by 2030: emergency services, mapping, imaging, inspection and surveillance within the applicable legal frameworks by civil drones, as well as the urgent delivery of small consignments, such as biological samples or medicines.

More information will be available soon...

More information will be available soon...

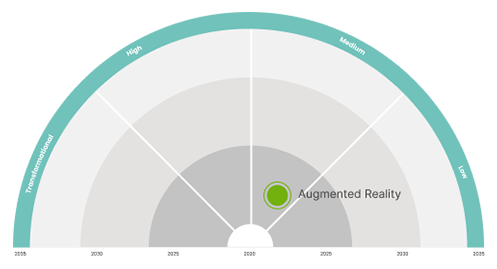

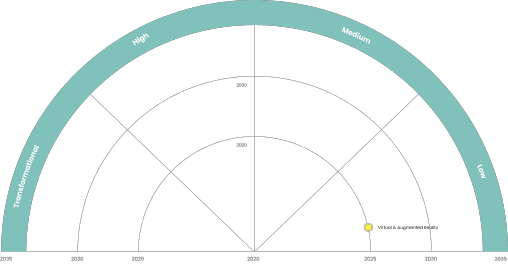

Virtual Reality (VR) refers to simulation technology, popularised by the gaming sector, which immerses a person in a digitally created artificial world, either realistic or imaginary. Other implementations such as Augmented Reality (AR) and Mixed Reality have also emerged. The current barriers, particularly in terms of reproducing the physical interaction (touch, force feedback, etc.) between the individual and the digital environment in which they are evolving, and the cost, are set to be overcome in the coming years.

According to Statista, revenue in the Augmented and Virtual Reality market is projected to reach US$8.02bn in 2023 and US$13.61bn by 2027. Increasing use of VR in instructional training, such as for field workers, engineers, mechanics, pilots, defence personnel, and technicians in various industrial sectors, is propelling the market’s growth.

More information will be available soon...

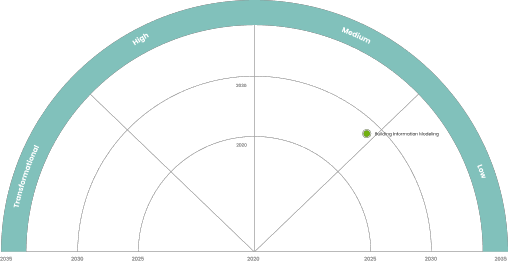

Building Information Modeling (BIM) is an approach to sharing information about a construction project throughout its life cycle, from design to demolition. The core of the approach is a structured, 3D digital model that brings together several types of information about the built asset. This digital model enables those who interact with the building to optimise their actions and maximise the overall value of the asset. This approach, which originated in the building sector, is now being extended to heavy infrastructure (bridges, ports, railways, roads) and to the energy sector (equipment, sites, networks). Thos is now known by many stakeholders as City Information Model (CIM) (not to be confused with the Common Information Model, CIM, standard developed by the electric power industry and officially adopted by IEC). BIM is a reality in the world of design and construction/renovation and is gradually being extended to the operational maintenance professions, becoming digital twins, with the acquisition of operational data.

The importance of energy analysis in building design has grown, but it is still mostly done by simple static calculations or estimates. By utilizing BIM as a data source for energy analysis, the data input will be more efficient and the existing data more reusable to perform accurate dynamic simulation to verify the thermal performance of buildings throughout their life cycle.

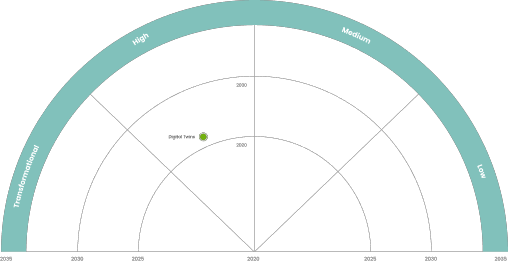

Digital twins are virtual replicas used for understanding, monitoring, diagnosing and forecasting installations, processes and, ultimately, an entire system such as the European electricity or energy system. Digital twins are emerging as future tools for improving performance through outage anticipation and increasing resilience through remote automatic control and near real-time decision-making support. Their aim is both to enable operations to be represented as closely as possible to reality, and to digitally capitalise on descriptive data about assets throughout the lifecycle of structures. Digital twisn includes four core technologies: the Internet of Things, simulations (using 3D modelling where appropriate), artificial intelligence, and cloud.

According to Fortune Business Insights, the world digital twin market size was valued at $8.60 billion in 2022 and is projected to grow from $11.51 billion in 2023 to $137.67 billion by 2030. The DSO Entity and ENTSO-E have signed a Declaration of Intent to develop a Digital Twin of the European Electricity Grid (December 2022) in the presence of the European commissioner Kadri Simson.

More information will be available soon...

European Distribution System Operators (E.DSO) promotes and enables customer empowerment and the increase in the use of clean energy sources through electrification, the development of smart and digital grid technologies in real-life situations, new market designs and regulation. E.DSO and its members are committed to taking on the huge challenges associated with realising the Energy Union, built on the EU’s ambitious energy, climate, security of supply, jobs and growth objectives. This involves ensuring the reliability and security of Europe’s electricity supply to consumers while enabling them to take a more active part in our energy system.

The current period is characterized by numerous and rapid technological developments and possible disruptions, particularly in the energy and Information Technology (IT) sectors. These transformations potentially have a significant impact on DSOs. They must therefore prepare for it, which sometimes imposes difficult choices between the subjects on which to work as a priority.

The Technology Radar's ambition is to evaluate technological topics that have a potential impact on DSOs and their ecosystem (public authorities, suppliers, customers, and employees).

The objectives are:

For each trend, a fact sheet has been drawn up summarizing the key elements relating to the technology considered, the developments in progress as well as the analysis of potential impacts for the DSOs. These may consist, for example, of a change in their business model, prospects for productivity gains or opportunities to develop new services.

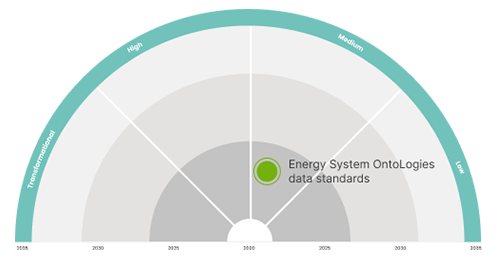

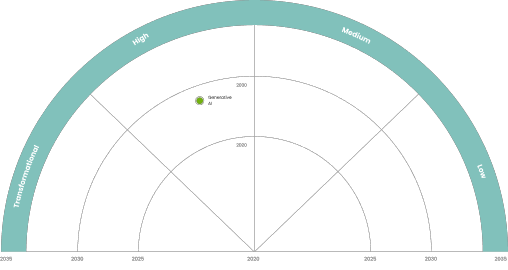

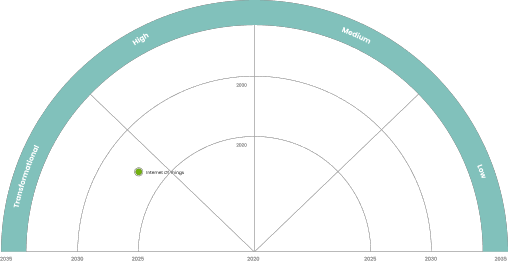

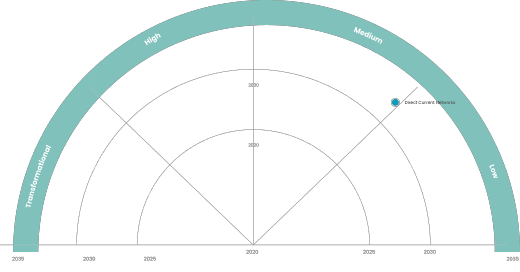

An aggregated view of all ongoing trends has been constructed by positioning each technology on a diagram according toestimates of industrial maturity time and magnitude of impact on DSOs. This helps to visualize key technologies as they relate to DSO activities.It should be noted that the position of each technology on this diagram is often only indicative and could be the subject of endless debate, in particular for technologies, such as artificial intelligence, which are already widely used and which however are subject to potentially disruptive new developments.

The trends analysed cover in particular energy systems, digital technologies, and the various emerging solutions serving operational performance.

A dedicated Task Force organized within the E.DSO Technology & Knowledge Sharing Committee and including high-level experts from a large set of European DSOs was set up to produce the Technology Radar. The sourcing and analysis of technologies has been facilitated by reaching, through the network of technology scouts, the best sources of information.

The members of the Task Force were:

Given the rapid evolution of technologies, E.DSO plans to carry out a regular update of its Technology Radar.

Last update: 28 September 2023

Generative AI refers to Artificial Intelligence and Machine Learning algorithms that use existing content to generate new content. Generative AI can generate text, sound, images, etc. Based on models stored in a database, it can produce its own similar model. For example, today's artificial intelligence systems can be trained to recognize a distribution network component in images, whereas Generative AI systems can be trained to generate an image of a distribution network component.

According to Bloomberg Intelligence, the generative AI market will reach $1,300 billion by 2032. It was close to $40 billion in 2022 and should reach $67 billion in 2023. The rapid growth of the generative AI market is best illustrated by the success of chatGpT. When it was launched in 2022, chatGpT had one million users in 5 days.

EU AI act with specific requirements on Gen AI will come soon (EU AI Act: first regulation on artificial intelligence).

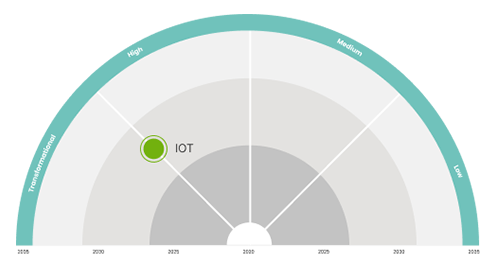

The Internet of Things (IoT) is an infrastructure of interconnected objects (mainly sensors and equipment), that contain embedded technologies to sense, communicate, process information, react and interact with each other or the external environment to create value from this interaction. IoT solutions encompass sensors, Information Technology (IT) and Operational Technology (OT) systems, communications, data storage and analysis, including AI. Increasingly, various industries are using IoT to operate more efficiently, deliver enhanced customer service, improve decision-making and increase the value of the business. With IoT, data is transferable over a network without requiring human-to-human or human-to-computer interactions.

IoT applications deal with numerous use cases: Human health (to monitor or maintain health and wellness), Home (home voice assistants, automated vacuum cleaners, security systems, etc.), Retail environments (Devices to facilitate self-checkout, extend in-store offers, help optimize inventory, etc.), Offices (energy management, security for buildings, etc.), Standardized production environments (to gain operating efficiencies or optimize equipment use and inventory), Custom production environments (to perform predictive maintenance and health and safety efforts), Vehicles (condition-based maintenance, usage-based design, autonomous vehicles, etc.), Cities (adaptive traffic control, smart meters, environmental monitoring, etc.). IoT solutions are already available and widely used. Their applications could sharply increase in the future with the development of edge computing and 5G.

Although the transmission and distribution of electricity is almost exclusively carried out in Alternating Current (AC), certain trends call for a reconsideration of the interest in Direct Current (DC): (1) renewable energy (photovoltaic, PV, and wind) and batteries (in particular electric vechicels) operate natively in DC, and the acceleration of renewable energy uptake reinforces this interest, (2) the proportion of energy consumed in DC at home is high (50% in 2018) and growing sharply (80% by 2030) and (3) innovation and falling costs in power electronics are making the use of DC increasingly economical.

The use of direct current could make it possible to limit conversions on the distribution network, be a source of simplification and improve the energy efficiency of the electrical system.

DC solutions, in particular for the distribution network, are raising great interest, with numerous demonstrators around the world and, as it appears, a proactive industrial policy in China. Standardization of DC networks is of critical importance (even more so for Low Voltage DC (LVDC) to enable the development of appliances). The International Electrotechnical Commission (IEC), and the Institute of Electrical and Electronics Engineers (IEEE) have all started standardization work on Medium Voltage (MV) and LV DC networks.

More information will be available soon...